|

Aspect |

Payment Gateway |

Payment Processor |

|

Role |

Captures and transmits payment data |

Authorizes and settles funds |

|

Customer-facing |

Yes |

No |

|

Handles funds |

No |

Yes |

|

RBI regulation |

Not required for pure gateways |

Required for aggregators handling funds |

|

Examples in India |

Razorpay gateway, CCAvenue |

Banks, card networks, NPCI |

How KwikAds helped Shop Unrush boost ROAS by 37% in 3 months

How KwikAds helped Shop Unrush boost ROAS by 37% in 3 months

How KwikAds helped Shop Unrush boost ROAS by 37% in 3 months

How KwikAds helped Shop Unrush boost ROAS by 37% in 3 months

Kwik Engage

Payment Gateway vs Payment Processor: What D2C Brands Must Know

07 Jun 2026

07 Jun 2026 15 Min Read

15 Min Read

Atul leads marketing at GoKwik, championing D2C brand building, growth strategies, scalable GTM for e-commerce, and data-driven customer acquisition. A former Amazon leader and IIFT MBA alumnus based in Bengaluru, he brings 15+ years scaling business across e-commerce, and fintech.

Read this blog on your favourite platform

Most D2C brands use "payment gateway" and "payment processor" interchangeably. That confusion costs money.

When you don't know which vendor controls what, you waste days troubleshooting with the wrong team when transactions fail. You negotiate fees with parties who have no authority to change them. You miss settlement delays until cash flow pressure forces you to notice.

Understanding the difference between a payment gateway and a payment processor determines whether you choose the right vendors, troubleshoot failures efficiently, and meet RBI compliance requirements.

This guide explains what each component does, where one ends and the other begins, and what D2C brands need beyond standard payment infrastructure to actually improve conversion and protect revenue.

What is a Payment Gateway?

A payment gateway is the customer-facing technology layer that captures, encrypts, and transmits payment data from the checkout process to the processing systems behind it.

It acts as the digital equivalent of a physical POS system, sitting between your merchant's website and the financial networks that approve transactions.

Every time a shopper enters credit card information or UPI details, the payment gateway handles everything that happens next. Here are the four core functions a payment gateway performs in every transaction:

- Encrypts card information and payment details using SSL protocols before transmitting them securely to the processor.

- Screens each transaction for fraud using behavioral signals and PCI DSS compliance controls to protect customer payment details.

- Runs 3D Secure authentication on high-risk card payments to verify the cardholder's identity before authorization proceeds.

- Routes the authorization request from the merchant's website to the appropriate payment processor or card network for approval.

In India, widely used payment gateway providers include Razorpay’s gateway layer, PayU, and CCAvenue across both large and small ecommerce businesses. Each of these platforms captures payment information at checkout and routes it for authorization.

Pure gateway solutions that do not handle merchant funds do not require authorization from the Reserve Bank of India. However, platforms that also manage fund settlement must operate under the RBI’s payment aggregator guidelines.

Also read: Best ecommerce payment gateways of the world

Also read: Best ecommerce payment gateways of the world

What is a Payment Processor?

A payment processor is the backend system that handles authorization, fund movement and settlement between the acquiring bank and the issuing bank. The payment processor never interacts with the shopper directly and operates entirely behind the scenes of every transaction.

Here is how the payment processor works across its four core functions in every approved transaction:

- It verifies credit card or UPI credentials by communicating with the relevant card network, such as Visa, Mastercard, or NPCI.

- It sends the authorization request to the issuing bank and receives the approval or decline response in real time.

- It moves funds from the customer's bank account to the acquiring bank after authorization is confirmed and recorded.

- It initiates the transfer of funds into the merchant's bank account on the agreed settlement timeline after batch processing.

In India, most D2C brands never interact directly with a payment processor because payment aggregators bundle processor and gateway functions.

Platforms like Razorpay, Cashfree, and PayU combine the entire payment process into a single contract, dashboard, and transaction fee structure.

This bundled approach simplifies onboarding, reduces integration effort, and allows brands to start accepting payments quickly without managing multiple vendors

What is the Difference Between Payment Gateway vs Payment Processor?

Here is a direct comparison of the payment gateway vs. payment processor across the most important e-commerce aspects for Indian D2C brands evaluating their payment infrastructure.

Under RBI guidelines, payment aggregators that handle merchant funds require authorization, whereas pure payment gateway technology providers operating without fund handling do not need approval.

This regulatory distinction determines which vendors your D2C brand must vet for PCI compliance and RBI licensing before committing to an integration.

This vetting process usually involves the following checks to ensure that your payment setup is compliant, before going live:

- PCI DSS compliance checks: Confirm that the provider is PCI DSS-certified and review its Attestation of Compliance to ensure secure handling of card data.

- RBI authorization status: Verify whether the platform is an RBI-authorized payment aggregator and operates in accordance with prescribed regulatory guidelines.

- Data security practices: Assess how payment data is encrypted and how tokenization is implemented to protect customer information.

- Settlement and reconciliation clarity: Understand how funds move to your account and how transactions are tracked and matched for accuracy.

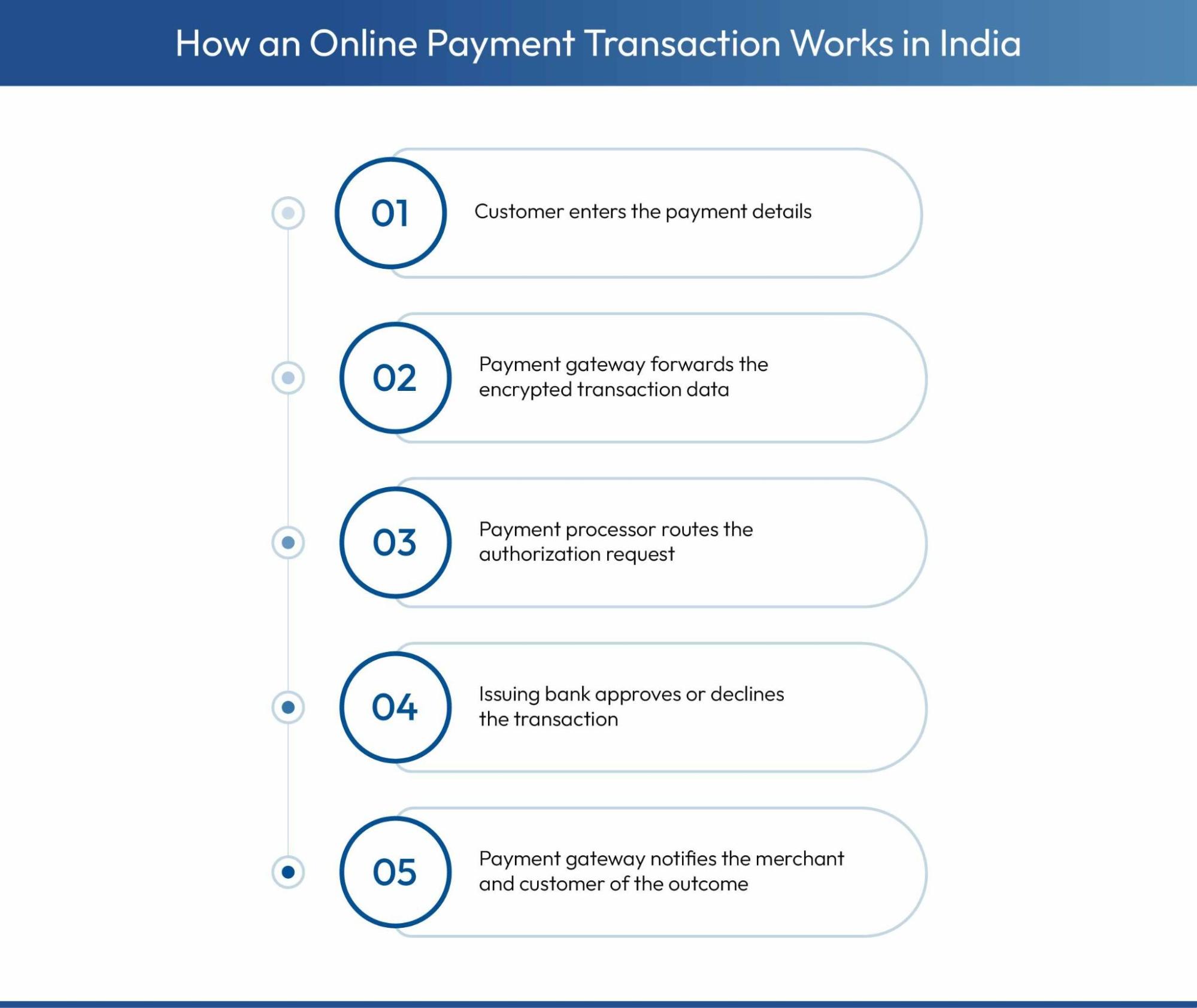

How does a Payment Transaction Work in India: Step by Step

Here are the stages that every transaction goes through before funds are credited in your merchant account:

- Step 1: The customer enters UPI or card payment details at checkout. The payment gateway immediately encrypts the data and prepares it for secure transmission to the processor.

- Step 2: The payment gateway forwards the encrypted transaction data and authorization request to the payment processor.

- Step 3: The payment processor routes the authorization request through the card network or UPI system directly to the issuing bank. This is useful for real-time balance and fraud checks.

- Step 4: The issuing bank approves or declines the transaction based on available funds and fraud signals. The response travels back through the payment processor to the gateway.

- Step 5: The payment gateway notifies the merchant and customer of the outcome. The payment processor initiates transfer of funds from the customer's bank to the acquiring bank for settlement.

How Does Understanding the Difference Between Gateway and Processor help?

When brands don't understand where the gateway ends and the processor begins, they waste time troubleshooting with the wrong vendor. Here are three common scenarios:

Scenario 1: Transaction failures during high-traffic events

Your flash sale starts. Transactions begin failing. You contact your payment gateway support team.

The gateway logs show everything worked correctly on their end-data was encrypted and transmitted successfully. The actual problem is at the processor level. The acquiring bank hit rate limits and started declining transactions.

But you didn't know to check there first. By the time you figured out which vendor actually owned the problem, you'd lost days of back-and-forth and high-intent customers who never came back.

When transactions fail, check both layers immediately. Ask your aggregator for processor-level decline codes, not just gateway error messages. "Transaction failed" tells you nothing.

"Declined by issuing bank - insufficient funds" tells you the customer needs to try a different card. "Declined by processor - rate limit exceeded" tells you the aggregator needs to route to a backup processor.

Scenario 2: Trying to negotiate fees with the wrong party

You want to reduce your payment processing costs. You reach out to your payment gateway contact to negotiate Merchant Discount Rate (MDR).

Three weeks of emails later, you learn the gateway provider has zero control over MDR. Those fees are set by the payment processor's relationship with acquiring banks and card networks.

You wasted weeks negotiating with someone who couldn't help you.

MDR negotiations happen at the processor or aggregator level, never at the gateway level. If you're using an aggregator like Razorpay or Cashfree, you negotiate with them directly, they control both layers. If you somehow have separate gateway and processor vendors, negotiate with the processor.

Scenario 3: Settlement delays with no clear owner

Your settlements usually arrive in 2 days. Suddenly they're taking 5 days. Your working capital is getting squeezed during a critical inventory restock period.

You email gateway support. They have no visibility into settlement timelines—that's controlled by the payment processor and acquiring bank. After multiple support tickets, you finally learn the processor flagged your merchant category for additional review, triggering automatic holds.

If you'd understood which vendor controls settlements, you would have escalated to the right team immediately instead of losing weeks.

Settlement issues are always processor-side issues. Gateways never touch funds. If money isn't hitting your account on schedule, contact your aggregator's settlement team or your processor directly. Don't waste time with gateway support, they can't see or fix settlement problems.

Payment Gateway vs Payment Processor vs Payment Aggregator: What’s the Difference?

In India, most D2C brands work with payment aggregators like Razorpay, PayU and Cashfree that combine payment gateway and payment processor functions under one contract.

This means one dashboard, one MDR rate, one settlement cycle and one RBI-compliance requirement covering the full payment stack for the brand.

Understanding how aggregators differ from standalone payment processor vs gateway setups helps brands evaluate vendor contracts and contingency options accurately.

According to RBI Master Direction on Regulation of Payment Aggregator (PA), payment aggregators must be Indian companies with a minimum net worth of ₹15 crore at application, scaling to ₹25 crore within three years of authorization.

This requirement does not apply to pure payment gateway technology providers operating without fund-handling authorization from the RBI under current payment card industry guidelines.

|

Basis |

Payment Gateway |

Payment Processor |

Payment Aggregator |

|

Primary role |

Encrypts payment data |

Authorizes and settles funds |

Combines both functions |

|

Customer-facing |

Yes |

No |

Yes |

|

Handles merchant funds |

No |

Yes |

Yes |

|

RBI authorization required |

No |

Yes |

Yes |

|

Indian examples |

CCAvenue, Atom |

Acquiring banks, NPCI |

Razorpay, PayU, Cashfree |

How to Evaluate Your Current Payment Infrastructure?

Run this audit quarterly to verify your payment setup is actually working for you:

Step 1: Map your actual payment flow

Open your aggregator dashboard and export last month's transaction data. For every 100 transactions, identify:

- How many were authorized by the gateway but declined by the processor

- How many failed at the gateway encryption step vs processor authorization step

- What your average time-to-settlement is by payment method (UPI vs card vs net banking)

If you cannot answer these questions from your current dashboard, you're flying blind. You don't know where failures are actually happening.

Step 2: Calculate your all-in payment cost

MDR is only one line item. Calculate the full cost:

All-In Payment Cost = MDR + Gateway Fee + Setup Fee + AMC + Chargeback Fee + Settlement Delay Cost

Settlement delay cost = working capital you can't access while waiting for funds to clear.

Example: If you're doing monthly revenue and your settlements take 4 days instead of 2 days, that's 2 extra days where your money is locked up instead of available for inventory, marketing, or operations. Calculate what that delay actually costs your business.

Step 3: Audit your processor relationships

Ask your aggregator these five questions:

- Which acquiring banks process our transactions? (You should have at least 2 for redundancy)

- What is our merchant category code (MCC) and is it optimal for our actual product category?

- Do we have direct processor relationships or are we pooled with other merchants?

- What triggers automatic settlement holds on our account?

- Can we get real-time processor decline reason codes, not generic gateway error messages?

If your aggregator cannot or will not answer these questions, you're paying for infrastructure you don't understand.

Step 4: Test your failure recovery capability

Simulate these scenarios and measure how long resolution takes:

- Gateway timeout during checkout → How many customers retry vs abandon?

- Processor decline due to suspected fraud → How long to whitelist a legitimate transaction?

- Sudden settlement delay with no notification → How long to get an explanation?

If you can't get clear answers within 24 hours, your current setup has gaps.

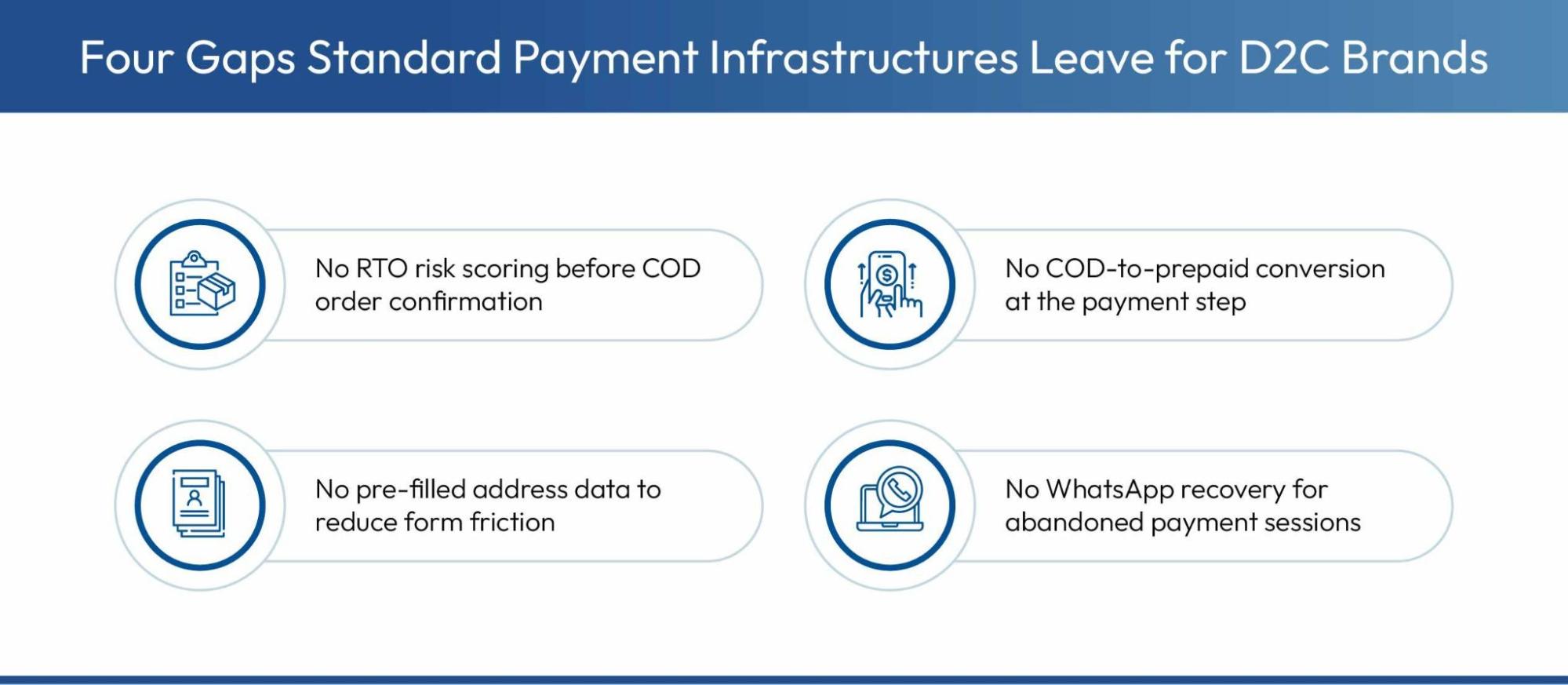

What D2C Brands in India Need Beyond a Gateway and Processor

A standard payment gateway processes the transaction, and a payment processor settles the funds.

This leaves four critical gaps unresolved for Indian D2C brands operating with high COD volumes and competitive checkout process expectations.

- Standard payment gateway services offer no RTO risk scoring on COD orders before the brand confirms dispatch, leaving high-risk orders indistinguishable from genuine ones at the point of authorization.

- Neither a payment gateway nor a payment processor converts COD-intent buyers to prepaid at the checkout process step. So, the brand absorbs the full RTO risk of every unverified cash order.

- Standard payment processing services include no pre-filled payment details or address data. This extends form completion time and directly increases drop-off rates on mobile app and desktop checkout sessions.

- No standard payment gateway or processor infrastructure includes post-abandonment WhatsApp recovery for shoppers who exit the checkout process before completing their online payments.

How GoKwik Goes Beyond Standard Payment Infrastructure?

Standard payment infrastructure handles authorization and settlement. It doesn't handle conversion.

Payment gateways and processors are not built to:

- Convert COD-intent buyers to prepaid before dispatch.

- Pre-fill verified customer data to reduce checkout friction.

- Recover abandoned payment sessions through post-checkout engagement.

- Flag high-risk RTO (Return to Origin) orders before order confirmation.

- Launch dynamic discounts or personalized offers to boost prepaid adoption.

- Run A/B testing on checkout flows to optimize conversion metrics.

These gaps exist because infrastructure providers focus on moving money securely, not optimizing for conversion. GoKwik's product suite addresses the revenue leaks that standard payment infrastructure leaves unresolved:

- Kwik Checkout runs a smart discounting engine that handles COD-to-prepaid conversion, RTO intelligence and network-level address pre-fill on top of standard payment processing from licensed aggregators. It converts paid and organic traffic at above-average rates while aligning each transaction with the brand's merchant account settlement requirements and margin targets across all payment methods.

- Kwik Pass gives returning shoppers a one-tap SSO login using their mobile number or Truecaller. This eliminates the account creation step that causes drop-off immediately after the payment gateway loads on mobile. Pre-filled payment details and address customer payment details from the GoKwik network compress the checkout process to under 10 seconds for over 85% of returning buyers.

- Kwik Engage recovers shoppers who reached the payment gateway page and abandoned it without completing online payments through automated WhatsApp flows triggered within minutes of exit. Multi-step recovery sequences with optional discount triggers convert these sessions into completed digital payment transactions. This is done without any manual effort from the brand team, recovering sessions that no standard payment gateway services platform addresses.

- GoKwik Cart surfaces prepaid incentives and upsell nudges within the cart view before the shopper reaches the payment gateway. This increases AOV and reduces COD dependency at the earliest possible funnel stage. Converting COD-intent buyers to prepaid before they reach the payment step reduces RTO exposure and improves transfer of funds timelines into the brand's merchant account.

- Return Prime manages the post-purchase journey by converting unavoidable returns into exchanges and store credit outcomes rather than cash refunds that permanently exit the brand ecosystem. This approach retains revenue per return event and strengthens customer experience at the stage where every standard payment gateway and payment processor solution stops without exception.

GoKwik closes every gap left open by standard payment infrastructure for Indian D2C brands.

Book a demo today to see how the full product suite converts more orders than any standard payment gateway or payment processor can deliver on its own.

Frequently Asked Questions

AUTHOR

Atul Bansal

Head of Marketing